For several months we’ve been anticipating that a slowdown in the real estate market was on the horizon, and with June’s numbers in, it appears that the shift has begun. What would ordinarily be the hottest time in the 2022 real estate market is in fact showing a decline in both median sales price and home sales, as interest rates impact would-be buyers’ bottom lines.

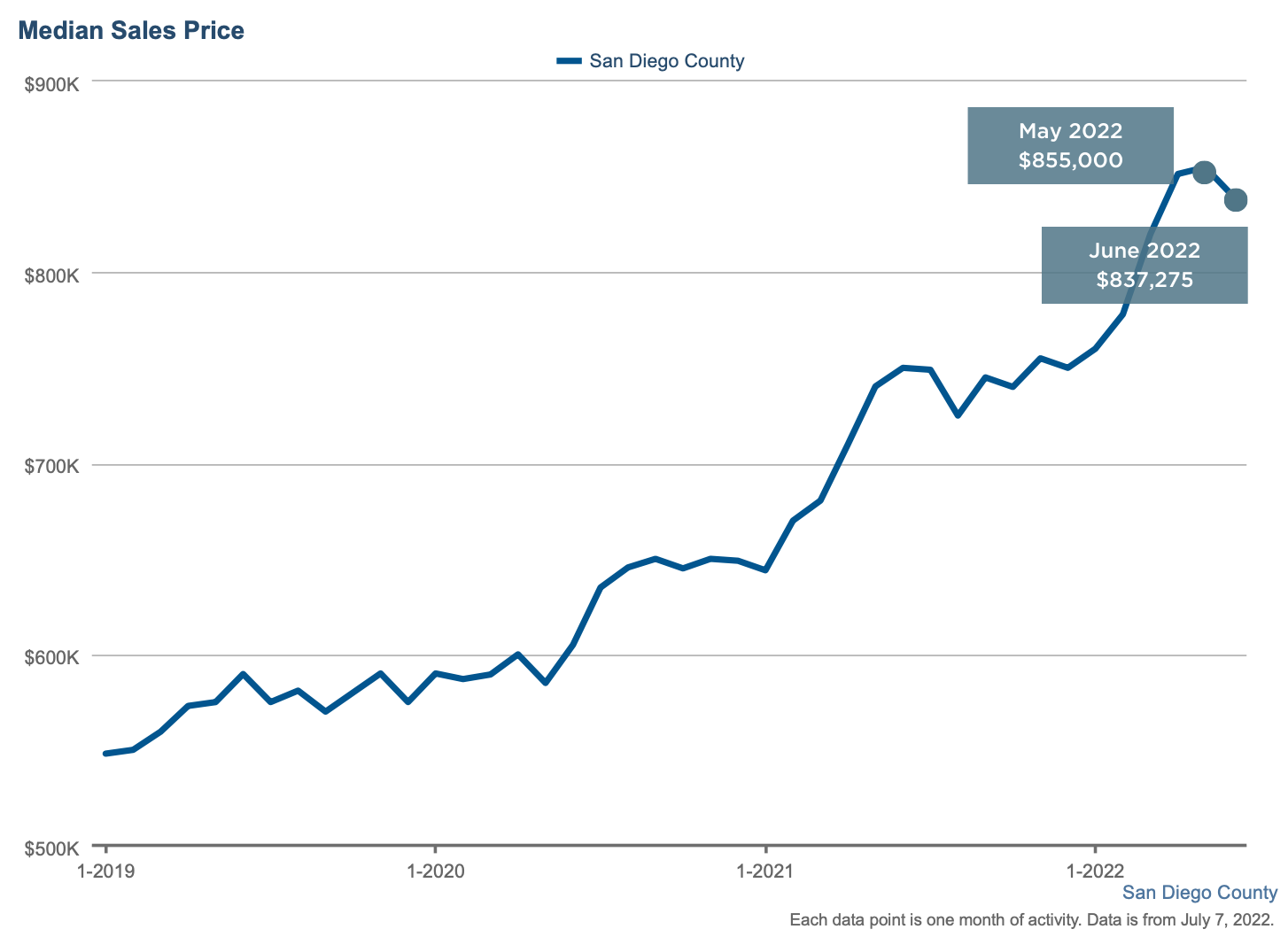

Median home prices for the month of June dropped slightly by 2% to $837,275 in comparison to the previous month’s median home prices of $855,000. Despite the small decrease median home prices are still up 11.6% to last year. Because of the continued imbalance of supply and demand for homes, we do not anticipate substantial price declines. In order to see dramatic decreases in home prices, we would need to see a very large increase in inventory. However, San Diego continues to experience a housing shortage with rents rising 10-20% annually and homeowners reluctant to sell their homes. While homeowners may be able to sell their home for more than it’s ever been worth, the price of a replacement home is also at an all-time high. Additionally, most homeowners locked in low interest rates on their mortgages while rates were below 3-4%. Now, with a higher interest rate environment, they are not eager to finance a replacement home at today’s rates.

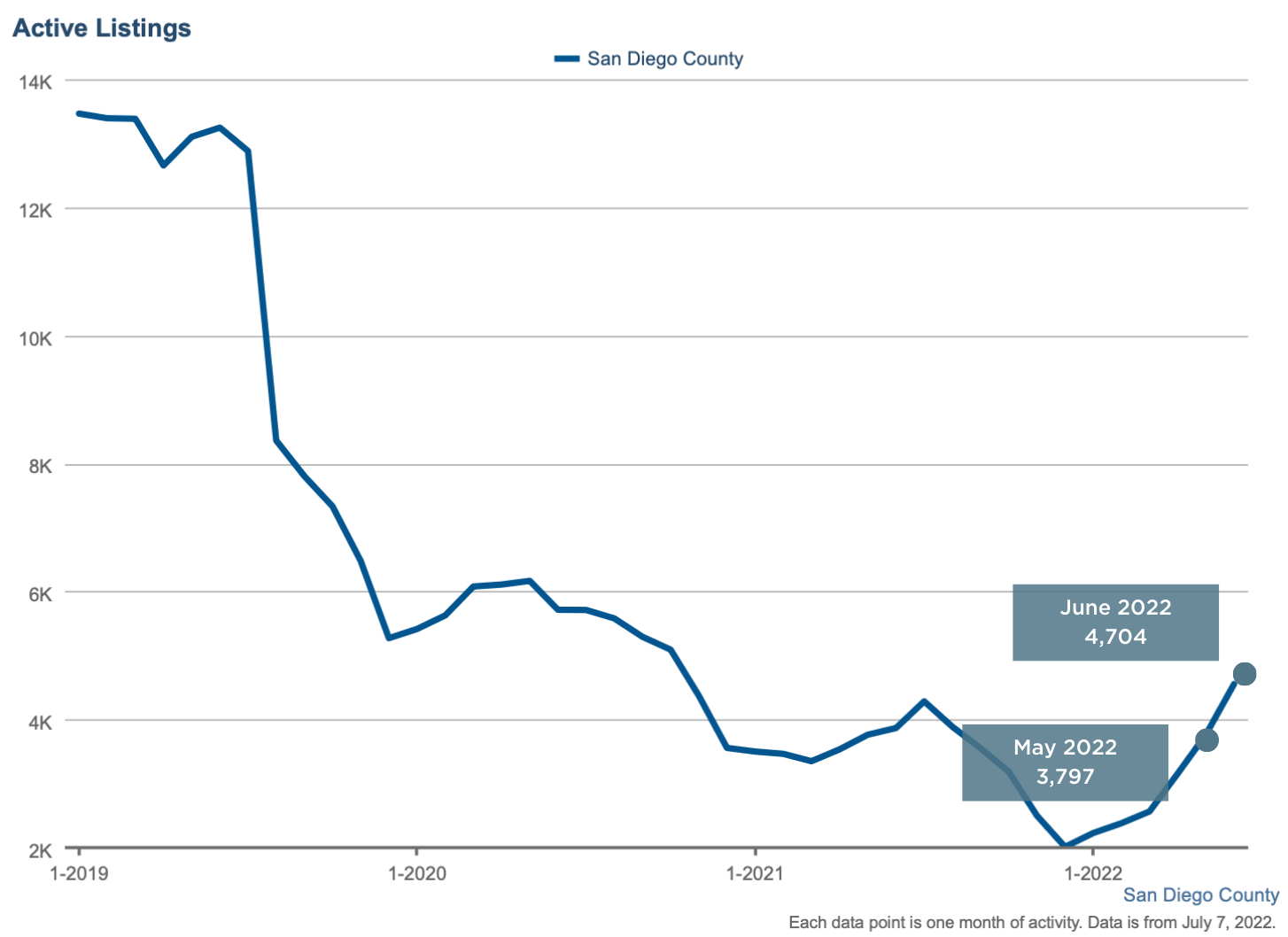

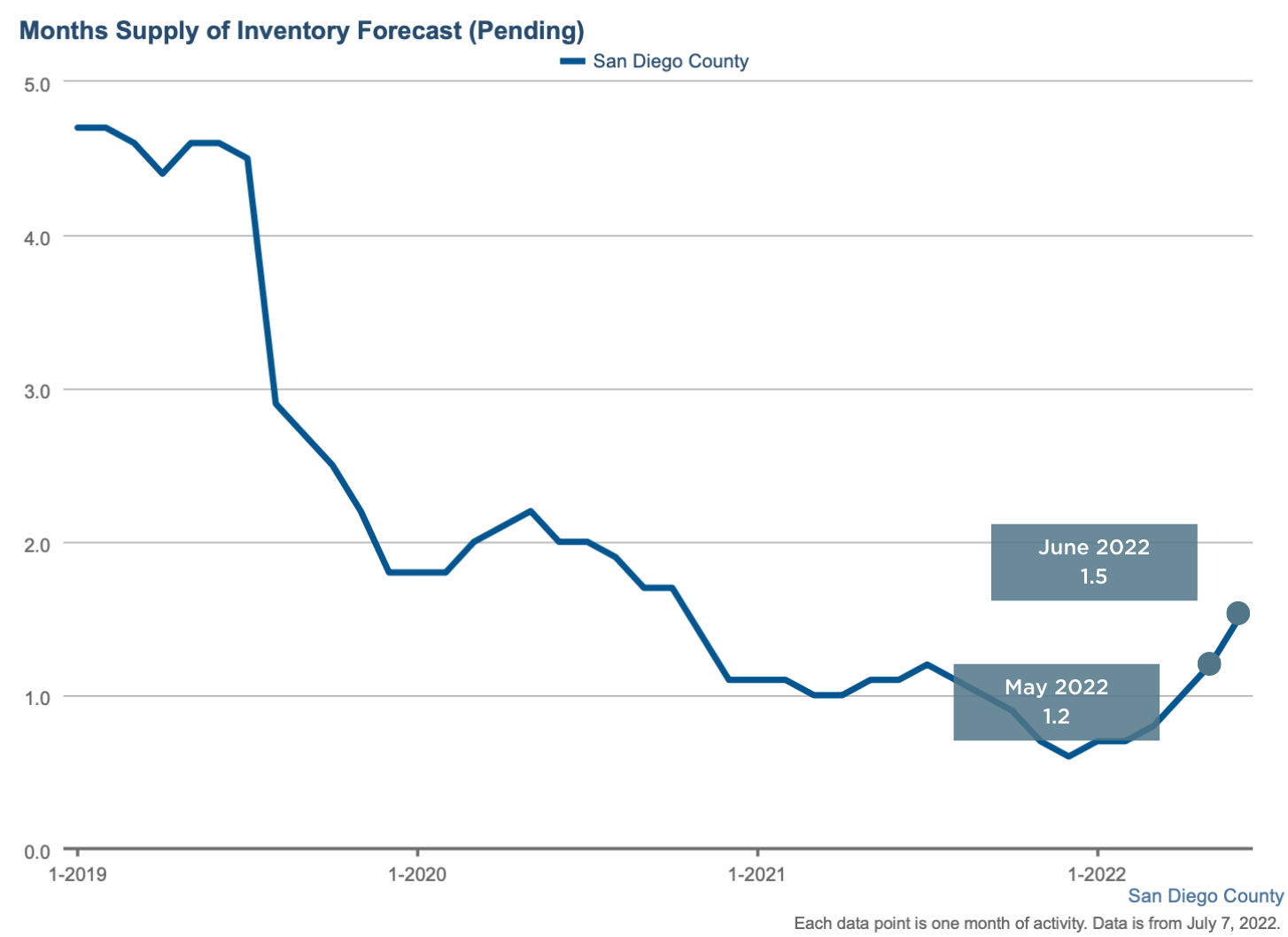

The number of homes for sale did increase by 24% to the prior month in part due to a small increase in the number of comes that came on market and this is the most number of active listings we have seen in over a year. However, it is still 65% less than we would normally see this time of year pre-pandemic.

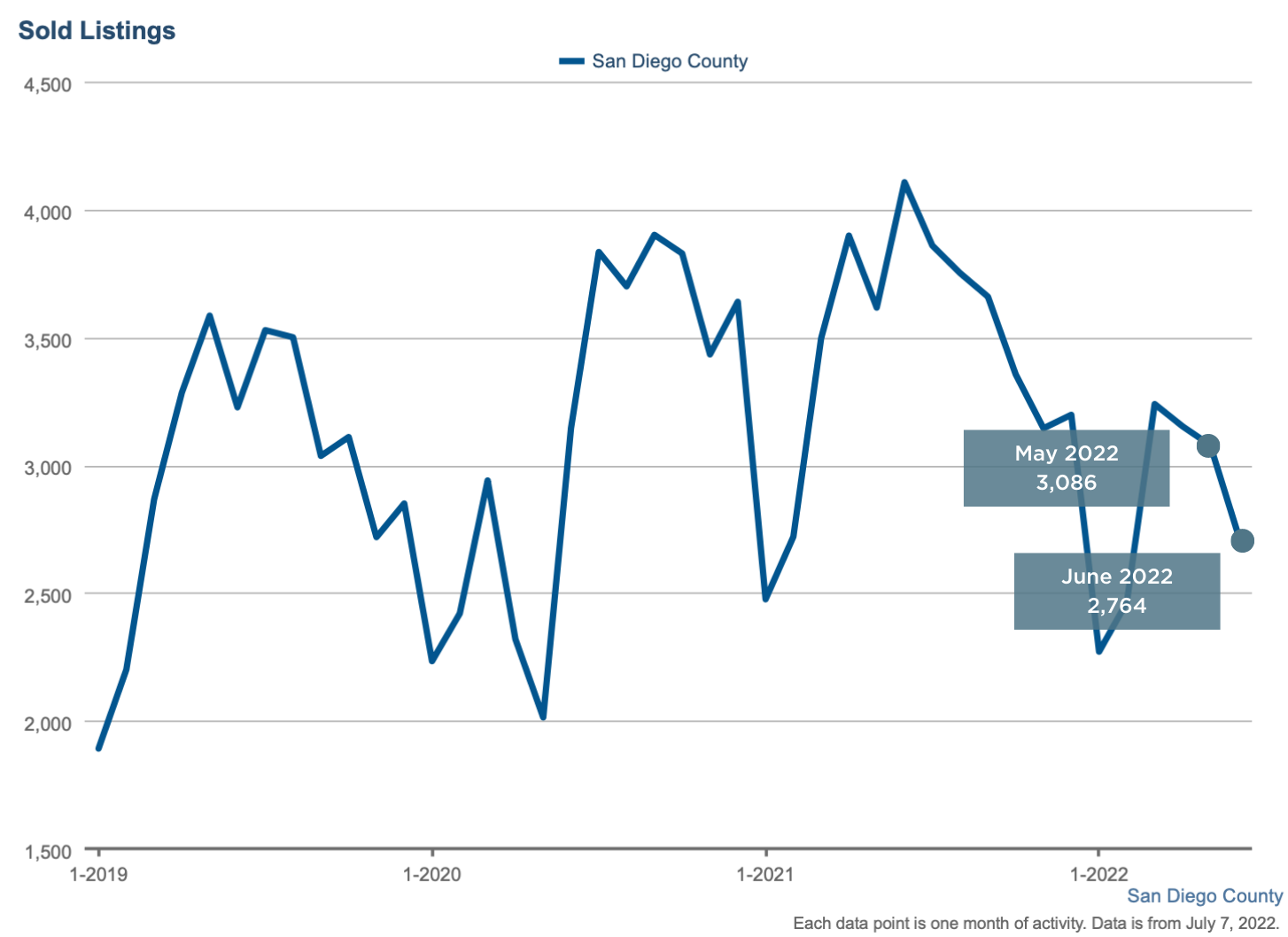

The driving factor in the increase in inventory was mainly due to the the 10% decline in the number of homes sold to the prior month and a decline of 19% in the number of pending home sales.

This is the first month we have seen buyer demand back off that much, our current market is a cooling off of the scorching buyer demand of the pandemic era. This shift in buyer demand is the intentional result of the Fed raising interest rates in order to reign in inflation, which is currently at a 40-year high. What’s interesting is that despite the 24% increase in inventory home prices have only been impacted by 2%, and it will be interesting to see how these numbers play out in the next few months.

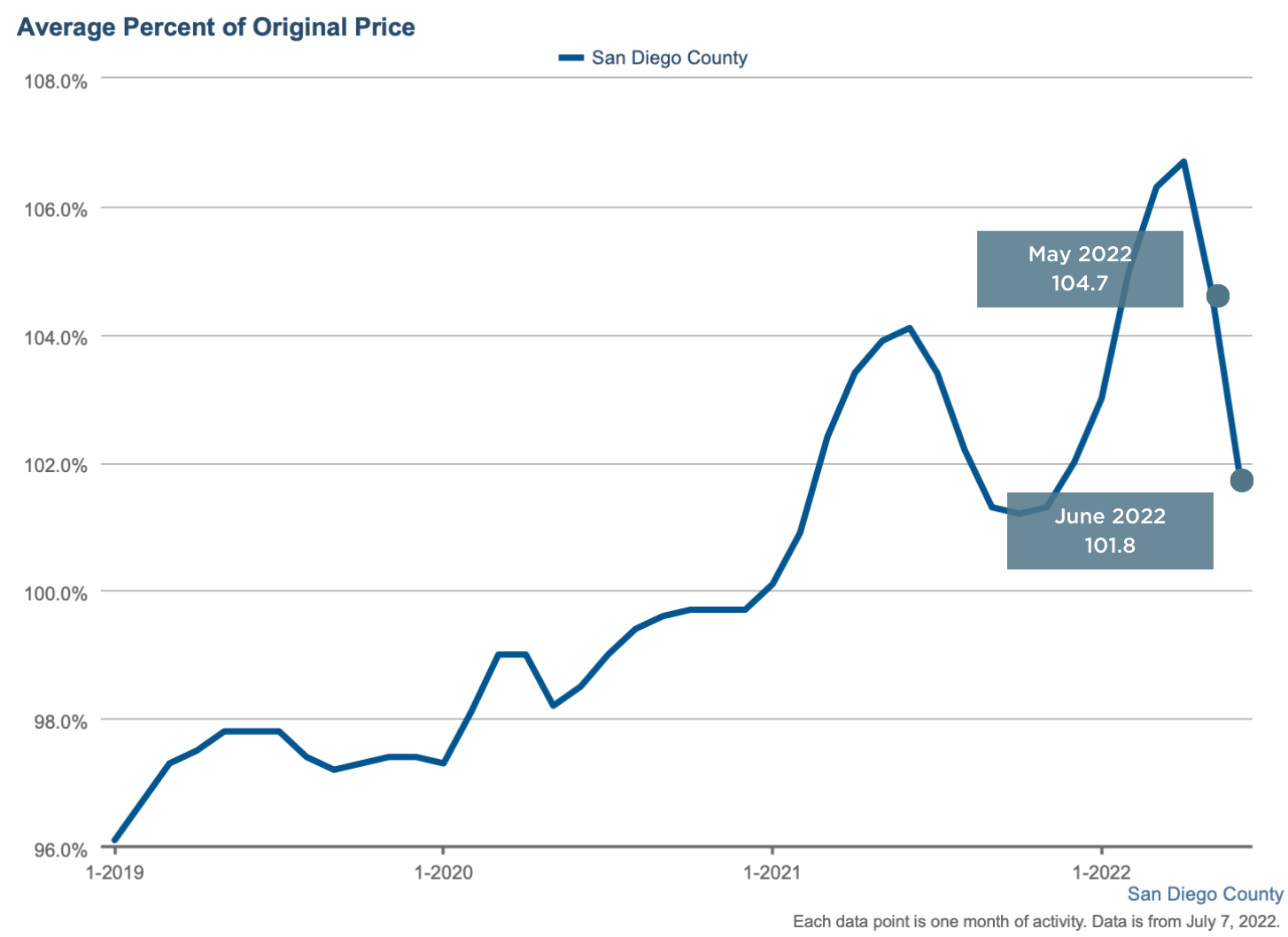

But for now we are seeing homes are staying on the market longer and we are seeing a decrease in the ratio of sales price to list price, which shows a substantial decline in bidding wars on homes for sale. The monthly mortgage payment of a median-priced home in San Diego using a 30-year fixed mortgage has gone up by nearly $1,400/month since December of 2021.

If you’re a homeowner:

Your equity is solid and you should not anticipate that your home’s value is going to drop substantially. You may see small monthly declines, but over the last 3 years your home has likely appreciated by 50% or more. You should, however, anticipate that the price gains you’ve been enjoying for the last several years may level out. You should also expect that the cost of accessing your equity via HELOCs and refinancing will, for some time, remain more expensive than it has been for the last decade plus.

If you’re considering selling your home:

It is likely that the Fed will continue to raise interest rates, at least through the end of this year. As a result we may continue to see decreases in buyer demand and some decreases in home values. Which is why it is now more important than ever to take the time to stage your home, market your property and price your home strategically to attract as many buyers as possible. We’re still seeing homes receive multiple offers and sell for over asking price, for those properties employing these strategies. Most importantly, you will still net an impressive return, even if you just bought your house as recently as last year, as home prices are still high and are up 11% to last year.

If you’re considering buying a home:

The decrease in the demand frenzy of the last couple of years is like a breath of fresh air for today’s homebuyers. We are seeing a substantial decline in multiple offers, it’s more like 2 or 3 competing offers versus the 10-20 competing offers we were seeing in the first half of the year. Homes are selling closer to their list prices and some sellers are willing to negotiate on price and terms. And the overpriced properties are taking price reductions. The challenge right now are the substantial interest rate hikes and the cost of buying using a standard 30-year fixed rate loan are higher than they have been in quite some time. That being said, there are many options to reduce your monthly payment including adjustable rate mortgages, rate buydowns, 11% down no-PMI loans and more. If you’re on the fence about buying because of interest rates, now is the time to explore alternative loan products.

As always, we will be here to continue to provide you with updates about the housing market and answer any and all of your questions. Feel free to reach out to us anytime.

|

||||||||||||||||||||||||

|